Ishita Shah | The Mobility industry in India has long eluded sustainable unit economics. Should we write it off?

:format(webp)/f/174198/1200x630/e838771b4d/mobility-landscape-india-ishita-shah.png)

Mobility has always been a large market in India. There are 48 cities with a population of over one million. The median age of India’s population is 28, which is well below that of 37 in China and the US. This implies that a large part of the population is young, earning incomes with no dependents, and therefore possesses a high disposable income. This generation is also more inclined to adopt technology and move away from asset ownership. Therefore, with rapidly increasing urban migration the mobility systems are being stretched at the seams.

If we look at the mobility market in India overall (Figure 1), a significant portion of passenger mobility needs is met by non-motorised modes of transport. This includes walking, cycling, and all forms of manual rickshaws or tuk-tuks. Railways is the most opted mode of transport for affordable long distance travel. However the overall share has fallen in the last decade owing to an increase in preferences for personal mobility options, i.e., four-wheelers for long distance travel. Two-wheelers and bus transport are still popular modes of transport by the number of kilometres traveled, given low costs.

Figure 1:* India’s total passenger mobility (passenger-kilometer) by modes of transport | Source:* CEEW

Figure 1:* India’s total passenger mobility (passenger-kilometer) by modes of transport | Source:* CEEW

If we zoom into the daily commute market, a staggering 95 million Indians use a vehicle for traveling everyday. Majority of these people (62%) opt for personal commuting options such as bicycles, two-wheelers and four-wheelers, whereas the rest (38%) take the bus, train or taxis (Figure 2). Together, the entire daily commute market is worth over US$ 83B.

Figure 2*: Mode of transport used by workers who travel using a vehicle (% people)| Source:* PGA Labs

Figure 2*: Mode of transport used by workers who travel using a vehicle (% people)| Source:* PGA Labs

Within these segments, road transportation (bus, two-, and four-wheelers) are more suitable for private sector participation while rail (trains, metro) and air transportation are more under government control.

We take a closer look at some of these segments below.

Personal Mobility

Within personal mobility, private car ownership in India is quite low, with only ~8% of households owning a car. Two-wheeler adoption is significantly higher with ~54% of households owning a scooter or a motorcycle. New business models are emerging in the following segments:

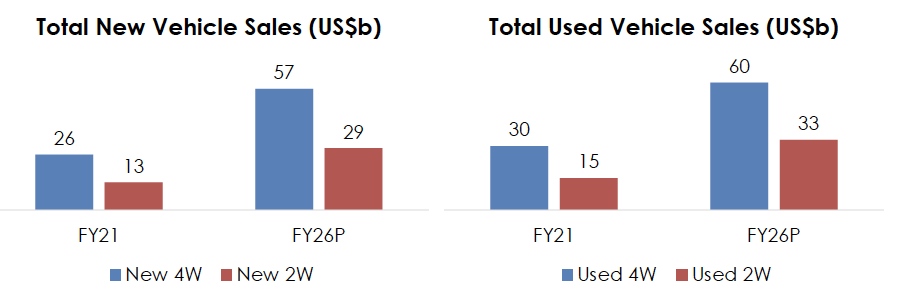

Used Vehicles

As the mobility market matures, demand for used vehicles is expected to grow. As of 2020, used vehicle sales have already surpassed the sales value of new vehicles for both four-wheelers (4Ws) and two-wheelers (2Ws) segments.

In 4W, full-stack used car models (like Spinny, Cars24, and CarDekho) have emerged over the last few years, with some of them going public within a few years since launch. Used 4W platforms raised a total of US$ 6B in 2021 alone. They have done the hard work of developing the market for used vehicle sales.

Used 2Ws is a more nascent market, better suited to e-commerce owing to lower selling prices, and customer’s quicker decision-making. Often the buyers are younger which implies higher digital purchasing behavior. Therefore, we believe the segment has the potential to grow. In terms of business model, the operational intensity in this business is fairly high, with several touch points with vendors and customers such as local procurement of vehicles, test drives, refurbishment, and home delivery. The model needs to be orchestrated carefully otherwise costs can quickly balloon, leading to excess inventory and poor economics.

Electric Vehicles (EV)

India is home to a staggering 22 out of the 30 most polluted cities in the world. With EV technology maturing and Total Cost of Ownership falling to compete with traditional Internal Combustion Engine (ICE) vehicles, policymakers are aggressively pushing for EV adoption. 84% of vehicles sold in India are 2W/3Ws, which are easier to electrify, owing to simpler battery requirements and vehicle structure. They are also much closer to economic parity on a TCO basis compared with cars or larger vehicles. Another sector which stands to benefit from EVs is intra-city logistics, where frequent deliveries bring down the per unit operating cost even lower than that of ICEs.

This opens up a large market for EVs covering manufacturers, infrastructure companies for battery swapping and charging stations, battery technology, and SaaS solutions for monitoring the lifecycle and health of both the vehicle and battery.

We do want to caveat that there is an inherent chicken-and-egg situation between charging infrastructure and EV adoption. With the initial push from the government, the ecosystem is maturing fast and we expect to see greater 2W and 4W adoption in the next few years.

Shared Mobility

There is a strong use case for investing in shared mobility as a way of supplementing existing public capacity available in rail and buses, and using technology to aggregate a small and fragmented supplier base across most modes of road transport.

Ride-Hailing and Micro-Mobility

4W ride-hailing businesses (like Uber, Ola) were the first models in shared mobility. They have been aggregating demand from consumers and leveraging partner-owned vehicles to build supply. We have seen that drivers are critical to the success of these models, and they need to be incentivized to deliver good customer experience.

2W micro-mobility businesses (Rapido, Yulu, or Bounce) came next, but for shorter distances and frequent use cases. However, their main challenges have been to ensure high asset utilization, and to manage the vagaries of distributed assets. Unit economics for both ride-hailing and micro-mobility businesses has remained elusive, owing to deep discounting that is needed to drive customer loyalty.

More recently, ride-sharing platforms with a fully electric fleet like Blu Smart have emerged, which can function on lower per unit cost. We are watching for other innovations in this sector.

Bus Commute

Buses are the cheapest and the most preferred mode of transport for long distances, comprising a whopping 43% of the US$ 83B market for daily commute. The private players make up 68% of this market, while public buses and contracted school buses make up for the rest. Businesses are trying to organize this market through various approaches.

- Ticketing: RedBus is a verticalized bus ticketing platform

- Full-stack asset-light approach: Aggregating private fleets and providing value-added services such as route discovery, online payment, and live tracking. Different companies focus on different routes, such as Cityflo for intracity and Chalo for intercity travel.

The main challenges stem from low per transaction AOV, i.e. the cost of the bus ticket, which makes it difficult to build sustainable unit economics. Driving effective capacity utilization and high retention of customers is key to this business.

Other mobility segments

Outside of passenger mobility, we look at two other segments in mobility, which are commercial logistics, and the enabling ecosystem of servicing, insurance and financing.

Commercial Logistics

Apart from passenger mobility, Logistics is another large segment which contributes to 13% of India’s GDP, higher than the global average of 9%. This is largely due to India’s land mass area and extensive long-distance transportation for domestic and export consumption. The market is fairly fragmented with over 90% of fleet owners in India owning less than 5 trucks. Business models in this segment involve:

- Fulfillment: Companies like Delhivery, which listed on Indian exchanges this year, and XpressBees, which is a Vertex portfolio company

- Inter-city Logistics: Trucking companies aggregating demand and building supply through both full-stack and aggregator models. I’m talking about companies like Rivigo and Blackbuck

- Intra-city Logistics: Companies like Shadowfax and Porter, operating light commercial vehicle-based fleets and building last-mile logistics

Alongside these, software solutions to manage and augment logistics operations have started scaling in India including solutions for navigation, fleet management, telematics, and fuel monitoring, among others.

The main risks which we watch out for are high attrition in supply (and manpower), and high costs of training which makes operating large fleets expensive. The prices are mostly well-discovered at a micro-market level, leaving wafer-thin margins for the taking. This necessitates very tight control on cost structures to get to operating profitability.

Aftermarket Servicing, Insurance and Financing

Around 30 million (~85%) cars in India are outside of OEM warranty, and roughly 65% of them get servicing done at local shops, unlike branded chains in developed markets. This presents an opportunity to digitize the supply chain and servicing segments. Some models include full-stack auto servicing models (like GoMechanic), digital solutions for auto workshops, and B2B trading of auto spare parts.

The adoption of auto insurance in India is on the rise. New-age digital insurers are using computer vision technology to develop objective assessments of the car condition. This helps capture an accurate account of the age, and characteristics of the vehicle which accelerates the underwriting process, and also assesses future risk. However, this technology is still in early stages, and technical accuracy and regulations on this are still unclear.

Verticalised EV financing is an emerging area, with the increasing adoption of electric vehicles. Given the amount of data that can be leveraged from sensors on the vehicles, newer underwriting models can be built, specifically for EVs. Traditional financial institutions also fail to separately value the battery. This gap can be filled in by new-age solutions (like Turno) that take into account the value of the battery in its second-life application, lowering the total cost of ownership of an EV.

Across servicing, insurance and financing, while digital behavior is on the rise, several components of onboarding and the customer lifecycle are still offline which makes it fairly expensive to acquire customers. This presents a key challenge in this business.

Where are we investing?

The mobility market is large and at an inflection point, and it is becoming likely that the traditional internal combustion engine vehicles will eventually be phased out, and be substituted by electric vehicles. This will bring about drastic changes in the entire mobility ecosystem and create opportunities for allied businesses. We are excited about the opportunities in EV financing, insurance, supply chain including manufacturing and aftermarket service, and of course, commerce opportunities in both retail and business segments.

The used vehicles space is also an interesting opportunity, especially for 2Ws. This market in its current form offers a broken customer experience, with a lack of any customer trust or loyalty.

It also bears to keep in mind that India is one of the largest markets for manufacturing auto components and ancillaries for domestic as well as export-led consumption. With the changes in the automotive landscape and the move towards more local and sustainable supply chains, we remain interested in any business models in this segment.

Lastly, spoiler alert: Vertex Ventures Southeast Asia and India (VVSEAI) recently invested in Beepkart, a marketplace for the purchase and sale of used 2Ws in India. More on that, here.

Do reach out to me at ishita.shah@vertexventures.com if you’re building in this space from India and Southeast Asia!

Read the original article on our medium here.

**For the latest news on Vertex Ventures SE Asia and India and our portfolio companies, follow us on Linkedin or** subscribe to our monthly newsletter.